to kill the Minotaur, but the true danger is not only the monster itself. It is the risk of losing all sense of direction inside a maze so complex that finding the way back becomes as difficult as the battle. This is where Ariadne’s thread matters: it represents the discipline needed to move through complexity without getting lost. In machine learning (ML), the visible challenge may be to beat a metric (the Minotaur), but the real risk lies in the maze built around it: hidden assumptions, fragile defaults, data leakage, misleading evaluation choices, unnecessary complexity, and preprocessing decisions that can make a model look stronger than it really is. This article follows that thread, focusing on how apparently strong results can emerge for the wrong reasons, and why maintaining methodological orientation is often more important than choosing the most sophisticated path.

Reality check

In ML, it is not unusual for an early prototype to produce striking metrics. At first sight, this may suggest that there is a real opportunity: the model seems promising, the signal appears strong, and the results look encouraging. But in practice, strong metrics alone do not mean that the model truly understands the underlying phenomenon, generalizes well, is robust, or is ready for deployment in a real-world environment. There are several methodological reasons why a model can appear much stronger than it really is.

This is especially concerning when candidates for data science roles are evaluated in HR or recruiting processes mainly through a checklist of tools, Python libraries, or AI buzzwords. That kind of screening may reward familiarity with the surface of machine learning while overlooking the deeper skill that matters most: the ability to question results, detect methodological flaws, and recognize when strong performance may be an illusion. If the problem is not the Minotaur itself, but the risk of getting lost in the maze built around it, then hidden assumptions, fragile defaults, and evaluation traps matter far more than the ability to recite tool names. In that sense, memorizing names is much easier than developing real scientific judgment.

As Catalini et al. [1] argue, the real bottleneck in an AI-rich world may shift from generating outputs to verifying them. In that sense, the central challenge is no longer just producing fast, low-cost code and convincing results, but developing the methodological discipline required to assess whether those results are genuinely trustworthy.

In this article, I aim to explain why striking metrics do not necessarily mean that a model is ready for deployment in a real-world environment. Phenomena such as data leakage, convenient metric selection, fragile default settings, poor split design, inappropriate cross-validation, target misspecification, uneven data coverage, sample imbalance, and preprocessing choices that hide instability or extremes can all create the illusion that everything is working well when it is not, regardless of the library or methodology being used.

To make these ideas concrete, I start with a case study that highlights common failure modes in time-series modeling under realistic data conditions. Additional examples could be explored later to further illustrate and extend these methodological concerns.

The case study is implied volatility forecasting with panel data. This problem aims to predict the market’s expectation of future variability embedded in option prices. It is particularly useful because it shows how target definition, panel structure, and date-level features can affect apparent predictability, induce temporal leakage under inconsistent validation schemes, and expose forecasting models to regime sensitivity.

Some hidden ML traps

Every algorithm is built on a set of assumptions and hypotheses that cannot be ignored. In an era where code is cheap, that intuition still matters: the real value lies not only in producing outputs quickly, but in knowing when results can be trusted, when assumptions are being violated, and when an apparently strong model is resting on fragile methodology.

In summary, my goal is to offer practical advice on the most common problems that weaken implementations in practice:

- The Default Pitfall: the passive acceptance of default options without examining the hidden risks, technical baggage, and assumptions they may carry.

- The Hidden Danger of Data Leakage: when information from unseen data enters model training, validation, or preprocessing through flawed splits, inappropriate cross-validation, or full-sample transformations, making performance appear better than it really is.

- The Mirage Metric: when an attractive performance metric gives the appearance of success while masking important weaknesses, such as scale bias, poor target alignment, or limited economic relevance.

- The Complexity Amplifier: when added complexity in the modeling pipeline increases fragility more than it improves real predictive performance.

- The Reversion-to-the-Mean Reality: when apparent predictive power is partly just natural return to average behavior (i.e., the tendency of unusually extreme values to move back toward more typical levels over time).

- The Free-Rider Problem: a governance pitfall in which the benefits of a model accrue to one party while the costs of failure are borne by another.

This is not intended to be an exhaustive list, but rather a set of examples that illustrate some of the hidden complexities in machine learning problems that can strongly affect their productivization and long-term success. For a more comprehensive review of common pitfalls in machine learning across different types of problems, see [5].

Implied volatility forecasting

Implied volatility (IV) is a measure derived from option prices that reflects the market’s expectation of future uncertainty or variability in the price of the underlying asset. It is important because it plays a central role in option pricing, risk management, and trading decisions, and is often treated as a forward-looking summary of market conditions.

For the implied-volatility case study, we use a dataset obtained from Kaggle containing daily SPY option-chain observations (2010–2018) from Options DX [4]. The data have a panel structure (that is, repeated observations of many individual option contracts over time), so each row corresponds to one option contract (option_id) observed on a specific date. The dataset included implied volatility (IV), Delta, days to expiration (DTE), S&P 500 index return (SPY_ret), and VIX values.

What follows is a set of pitfalls that should not be seen as independent technical errors, but as interconnected mechanisms through which a model can appear more reliable than it really is.

Default pitfall

In behavioral economics, this is typically described as status quo bias or a default effect: decision-makers disproportionately remain with the preselected option, even when switching is easy and the framing should, in principle, be irrelevant [2]. In machine learning, an analogous problem arises when default settings are treated as if they were methodologically neutral. They are not. Defaults encode assumptions about the structure of the data, the objective of the task, and the meaning of good performance.

The implied-volatility (IV) case illustrates this clearly. Option-panel data are not a standard tabular problem in which rows can be safely shuffled before splitting. Observations are grouped by date, contracts with similar strike prices and expiration dates are strongly related, and market-wide predictors such as SPY return and VIX are shared by all contracts observed on the same day. Under these conditions, a default random split with shuffle=True is not an innocuous choice: it can place contracts from the same date in both training and test sets, allowing the model to exploit shared market structure rather than learn relationships that genuinely generalize through time [3].

A second issue concerns the passive reliance on generic library settings during model development. Default hyperparameters are designed as broad starting points, not as guarantees of suitability for a specific dataset. In the IV setting, this matters because the apparent performance of more flexible models (such as neural networks and XGBoost) depends strongly on how evaluation is designed. Hyperparameter tuning may be necessary, but it must be carried out without contaminating the final holdout. Once the test set is used to guide model selection and is then reused for final reporting, it no longer serves as a valid out-of-sample benchmark.

Default pitfall also appears when default choices impose assumptions that are poorly aligned with the problem. Standard regression metrics such as MSE reward numerical closeness, yet in this setting that may not coincide with the more meaningful forecasting question, such as capturing relative IV changes or the correct direction of movement across contracts. Likewise, standard ML workflows often behave as though the data were iid, even though option-panel observations are temporally ordered, cross-sectionally dependent, and regime-sensitive. In that sense, defaults become dangerous not because they are always wrong, but because they are too easily mistaken for neutral choices when they may be structurally misaligned with the forecasting task.

The Hidden Danger of Data Leakage

Under data leakage, performance metrics may look excellent, but they are misleading: rather than measuring true predictive ability, they capture the model’s indirect access to information that would not be available in a real forecasting setting. I discuss this more broadly in [6].

To demonstrate the effects of data leakage, we reproduce the experiment of Arratia et al. [3]. We follow the same modelling logic: contract-level observations indexed by option_id and date, standard explanatory variables (spy_ret, delta, dte, vix), and a one-step IV-change target. Specifically, our primary training target is target_diff = IV_t − IV_{t-1} computed for different models and different number of variables: two-feature (SPY_ret, Delta), three-feature (SPY_ret, Delta, DTE), and four-feature (SPY_ret, Delta, DTE, VIX).

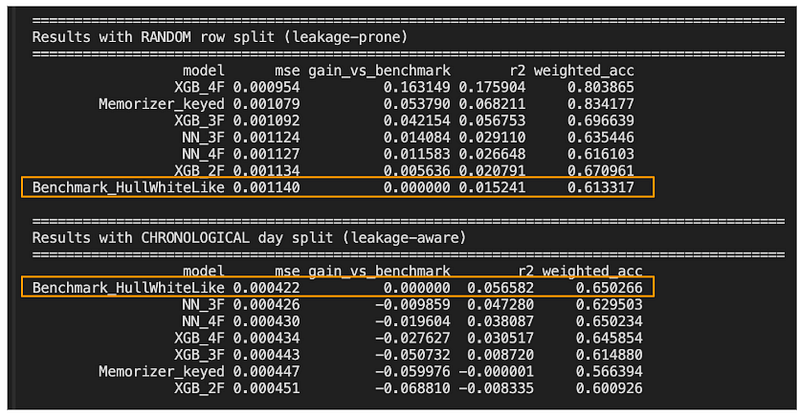

In Figure 2 we can see:

- In random split, complex models (especially XGBoost) show apparent gains and better R²/weighted_acc. In chronological split, that advantage falls or disappears; several complex models remain below the benchmark (negative gain).

- This indicates that part of the performance in random came from shared train-test structure (same date / same daily market information), not from a real ability to generalize to the future.

- Adding features does not guarantee robust out-of-sample gains once split is leakage-aware.

As you can see in Figure 2, there are two baselines in the experiment (one of which will be discussed in more detail in the following sections). The memorizer keyed baseline is intentionally simplistic: it does not model implied-volatility dynamics, but simply stores the average target associated with repeated date-level keys (SPY_ret, VIX). Its purpose is diagnostic rather than predictive.

- Because the IV variables are largely day-level signals shared across many options, random row-wise splits often place highly related observations from the same dates in both training and test sets. As a result, memorizer keyed baseline can achieve deceptively strong test metrics by matching repeated keys rather than learning true out-of-sample dynamics.

In Figure 2, it is clear that under the random row-wise split, memorizer keyed baseline performs surprisingly well, which suggests that the model is benefiting from repeated same-day information rather than learning genuine forecasting dynamics. Once the data are split chronologically, that advantage disappears: its performance drops, this pattern indicates that its apparent strength under random splitting was largely driven by leakage-like overlap rather than true predictive skill.

The Complexity Amplifier

Under leakage-prone or otherwise permissive validation schemes, more complex models can appear to outperform this benchmark by a wide margin. However, part of that apparent superiority may come not from a deeper understanding of the volatility process, but from their greater ability to absorb spurious structure, shared date-level information, or repeated market conditions. Once the split is made time-consistent and the evaluation protocol is corrected, the advantage of NN and XGBoost shrinks sharply and may even disappear. The point is not that complex models are inherently worse, but that their flexibility can amplify methodological flaws and make weak evidence look like strong predictive power.

A similar caution applies to time-series foundation models (TSFMs), which promise zero-shot predictions without the need for training or fine-tuning. Their appeal comes precisely from the fact that they are pretrained on broad collections of time series drawn from multiple datasets. Meyer et al. [7] indicate that the evaluation of TSFMs is especially vulnerable to information leakage through both (1) direct train–test sample overlap, where identical or near-identical samples reappear across training and evaluation data, and (2) temporal overlap across correlated series, where different series still share related time structure. The risk is that these pretrained models may exploit repeated structure and shared temporal information from source datasets whose exact composition is often unclear to the end user, making weak validation look like genuine forecasting progress.

This is where the importance of a baseline matters. A strong baseline is valuable not because it is simple, but because it provides a meaningful reference point for judging whether added complexity truly delivers incremental value. In the implied-volatility setting, a baseline such as the Hull and White minimum-variance-delta framework (Figure 3) is especially useful because it is economically interpretable, grounded in domain logic, and aligned with the structure of the problem. Choosing a good baseline matters because weak baselines make almost any sophisticated model look impressive, whereas a strong baseline forces the comparison to be honest. If a complex model only outperforms a trivial benchmark, the result says little; if it cannot consistently beat a well-chosen, theoretically motivated baseline under leakage-aware evaluation, then its apparent gains are unlikely to reflect genuine predictive progress (see Figure 2). In that sense, the quality of the baseline determines the quality of the claim.

Additionally, reformulating the problem as classification rather than regression is often inherently easier, since predicting the direction of change is less demanding than predicting its exact size. More broadly, complexity should be justified by the business objective, not by the availability of powerful algorithms. When the real goal is to support a practical decision rather than estimate an exact quantity with maximal precision, a simpler formulation may be more appropriate and more robust. Otherwise, added complexity can become self-defeating: it increases methodological fragility without delivering proportional business value.

Yet even when baseline or model choices are appropriate, model comparisons can still be distorted by the way success itself is measured.

The Mirage Metric

The Mirage Metric becomes especially visible in implied-volatility forecasting when Mean Squared Error (MSE) is treated as the main criterion of success. A prediction that gets the direction of the IV move right may still receive a worse score than one that is numerically closer to zero but points in the wrong direction. In that sense, MSE can reward numerical closeness over forecasting usefulness, masking problems such as poor target alignment and limited economic relevance.

The choice of target further affects how MSE behaves:

- Raw differences measure changes in absolute IV points, whereas

- log-differences measure changes relative to the starting IV level.

These two formulations are not economically or statistically equivalent. In this setting, log-differences can be more meaningful because they reduce the scale bias introduced by raw IV changes, under which high-IV contracts contribute disproportionately to the total error. As a result, the model may place too much weight on high-IV options even when a smaller absolute move in a low-IV contract is equally or more important in relative terms.

For this reason, the analysis goes beyond raw IV differences and also considers log-differences, directional classification, and weighted accuracy as more informative ways to evaluate model quality.

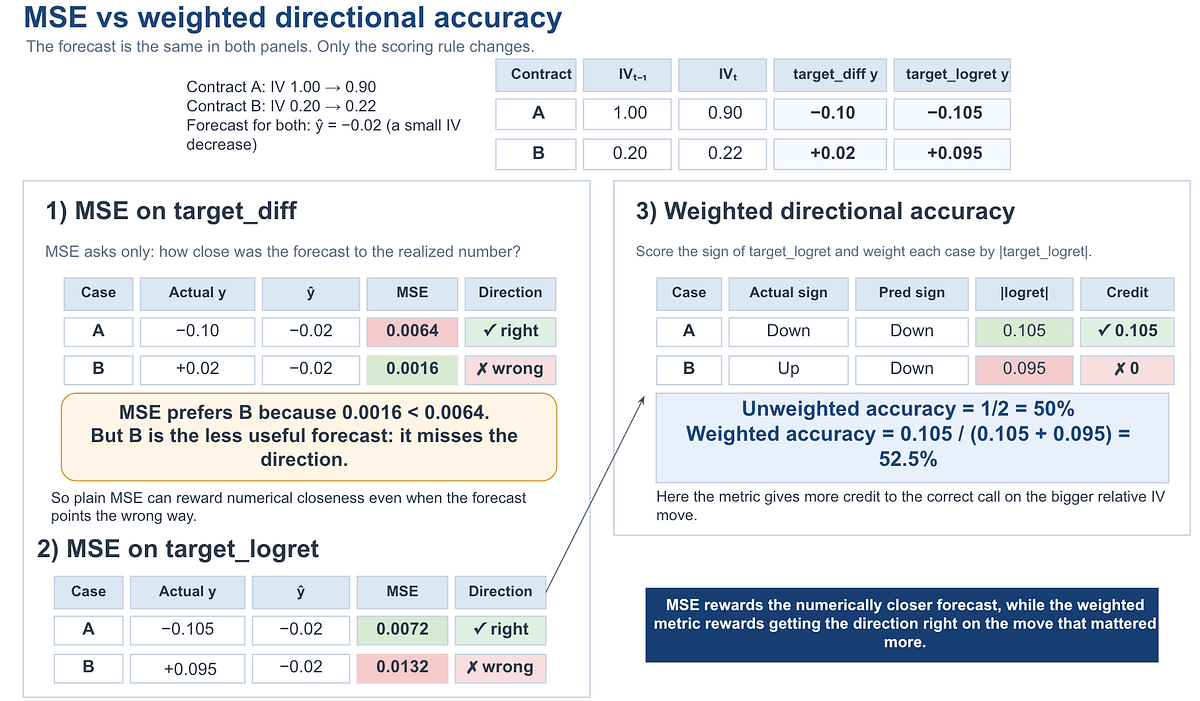

Figure 4 uses a single example to illustrate two closely related ideas. Two contracts experience different realized IV moves. Contract A falls from 1.00 to 0.90, while Contract B rises from 0.20 to 0.22. Suppose that the model produces the same forecast in both cases:

- With target_diff, MSE prefers Contract B because the prediction is numerically closer to +0.02 than to −0.10, even though B gets the direction wrong and A gets it right. This contrast is also highlighted by the color coding in the figure.

- When the same realized moves are instead expressed as log-returns (

target_logret), the target becomes more comparable across contracts because it reflects relative rather than absolute movement, and MSE now prefers A rather than B. - Finally, once

target_logretis fixed, the weighted directional metric goes one step further: it scores whether the model predicts the correct direction and gives more importance to larger relative moves. In this example, A receives credit because the forecast correctly predicts a downward move, while B receives none because the forecast misses the sign.

The main lesson is that both the definition of the target and the choice of metric can materially change which forecast appears to be “better.”

Mean reversion

Mean reversion refers to the tendency of unusually high or low values to move back toward a more typical level over time. In the implied-volatility setting, this means that if current IV is high relative to its recent history, the next change in IV may tend to be lower or even negative; conversely, if current IV is unusually low, the next change may tend to be higher. This does not necessarily imply a full understanding of volatility dynamics, but it does suggest that part of the signal may come from a simple normalization effect.

A more precise concern, however, is not regression to the mean in isolation, but the way methodological choices can amplify it. When many observations share repeated values, or when predictors are constructed through averages, medians, or other aggregated summaries, variability may be compressed and local heterogeneity may be hidden. In that sense, a model can appear more predictive simply because it is exploiting shared structure, normalization dynamics, or central tendency rather than learning a richer and more durable relationship.

In other words, the issue is not that implied volatility lacks signal, but that a poor experimental design can overstate how much of that signal the model truly understands.

The Free-Rider Problem

Finally, although this is perhaps less related to the methodological setup, I want to highlight another issue that is equally important: the Free-Rider Problem. This arises when incentives are misaligned so that one party captures the gains while another absorbs the costs or downside consequences.

This creates perverse incentives: those in charge of evaluating success may reward for faster deployment, better headline metrics, or apparent short-term gains, while the operational, regulatory, financial, or reputational costs of failure are shifted to the operations teams and customers. In practice, metrics can stop reflecting real value and start rewarding what is easiest to measure or easiest to report, which can discourage honest communication about limitations, uncertainty, or maintenance needs.

This creates perverse incentives: those in charge of evaluating success may reward faster deployment, stronger headlines or metrics, while the operational, regulatory, financial, or reputational costs of failure are borne by operations teams, customers, or other parts of the organization. In this sense, metrics can stop reflecting real value and may discourage honest communication about limitations, uncertainty, and long-term maintenance needs.

Conclusion

The issues covered here should not be seen as an exhaustive list, but as part of a wider and interconnected set of concerns that shape whether a model is genuinely reliable or only appears so. Future articles will extend this discussion to other methodological challenges, including coverage bias, hidden data contamination, spatial autocorrelation, regional heterogeneity, aggregation bias, and the tension between statistical accuracy and economically meaningful evaluation.

References

[1] Catalini, C., Hui, X., & Wu, J. (2026). Some simple economics of AGI. https://arxiv.org/abs/2602.20946

[2] Samuelson, W., & Zeckhauser, R. (1988). Status quo bias in decision making. Journal of Risk and Uncertainty, 1, 7–59.

[3] Arratia, A., El Daou, M., Kagerhuber, J., & Smolyarova, Y. (2025). Examining challenges in implied volatility forecasting: A critical review of data leakage and feature engineering combined with high-complexity models. Computational Economics. https://doi.org/10.1007/s10614-025-11172-z.

[4] dudesurfin. (n.d.). SPY Options EOD Data (2010–2023) [Data set]. Kaggle. https://www.kaggle.com/datasets/dudesurfin/spy-options-eod-volatility-surface-2010-2023.

[5] Lones, M. A. (2024). Avoiding common machine learning pitfalls. Patterns, 5(10), 101046. https://doi.org/10.1016/j.patter.2024.101046

[6] Gomes-Gonçalves, E. (2025, September 15). No peeking ahead: Time-aware graph fraud detection: Leak-free graph fraud detection. Towards Data Science.

[7] Meyer, M., Kaltenpoth, S., Zalipski, K., & Müller, O. (2025). Rethinking evaluation in the era of time series foundation models: (Un)known information leakage challenges (arXiv:2510.13654). arXiv. https://doi.org/10.48550/arXiv.2510.13654